What are the three warning signs that a business is on the verge of failing?

“Failure isn’t fatal, but failure to change might be”

John Wooden – American basketball player and coach

Sadly, hundreds of businesses collapse each year in Australia, often owing millions to creditors and employees.

As a business owner or manager, what are the warning signs?

Please remember, we have to be honest with ourselves, have an open mind and put egos and denial aside.

“Confront the brutal facts”. This is what Jim Collins says in his book Good to Great.

Here are 3 warning signs that a business may fail:

- Revenue is dropping

As a manager or business owner, measuring revenue and recording it month by month over a significant period of time for at least 2 to 3 years is critical in understanding and managing the business. Many businesses have seasonal fluctuations. For example, retailers’ revenues peak before Christmas and chocolate manufacturers’ peak before Easter. It is important to understand the nature of your business.

Understanding the fluctuation in sales over the year allows you to manage your cash flow.

There is an extremely important principle in business that is often misunderstood:

“Revenue is different from sales as revenue is money collected”

A sale is not a ‘true’ sale until you collect the revenue. It is important to have a cashflow forecast combined with sales and revenue recording in order to understand the implications and relationships.

A sudden drop in revenue could result in a business not meeting their legal obligatory costs such as superannuation payments and tax payments. This is a warning sign that the business is in trouble.

I once saw a business claim to have increasing sales to a major retailer only to find out that most of the sales were on a sale or return basis. This business went broke.

- Cash Flow Shortage

Many businesses can be profitable but fail due to running out of cash to pay their creditors. Cash is the lifeblood of any business. For example, sales and profit may be increasing, but due to not being able to collect the sales revenue in time, the business runs out of cash.

Here is a second important principle that needs to be understood:

There is a massive difference between profit and cash.

It is therefore very important to forecast and track cashflow. By using a cashflow budget, the discipline of collecting from debtors monthly can more easily be implemented. Running out of cash is a good indication that a business is in trouble. Debtors who are slow payers and are a significant proportion of a business’ sales can put the business at risk.

Alternatively paying creditors later can significantly improve a business’ cash flow and provide funds for expansion.

In our logistics business we tracked our cash needs 6 months ahead and then tracked them against our actual performance. Wages were over 35% of our overall costs. In Australia, wages are normally paid weekly whilst collecting from creditors takes between 30 and 45 days. A single decision to outsource our production labour with 30 day payments terms released cash into the business negating the requirement to seek external finance to grow the business.

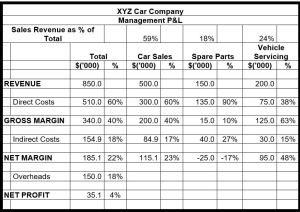

- Opaque Accounts

Sadly, many business owners do not understand their accounts. Many rely on their external chartered accountant to provide them with their profit and loss figures, which are often not delivered in a timely manner. Accountants tend to report profit and loss in terms of tax compliance and rarely do the accounts provide an operating perspective.

There is a third important principle for managing business accounts:

“Variable costs, fixed costs and overheads must be clearly identified in the profit and loss statement”

I had a client whose accounts were prepared and forwarded by their external accountant up to 3 months after the end of month. The business had no idea what was making a profit. They only knew that the business made a profit. Following some discussions and correctly categorising costs into variable, fixed and overheads, we determined that there were actually three businesses or sub-businesses and that only one was making a profit.

We immediately engaged a book keeper, broke the business reporting into the three businesses and set up the accounts to reflect the operating environment. Within 6 weeks, the owner was receiving P&L information within 3 days from the end of the month. In 9 months the business had grown 50% as they could concentrate on the areas where the business was profitable. The owner now knew their gross margins, breakeven points and profits.

What are the lessons?

While the three warning signs of business failure are financial, there are two other non-financial reasons for business failure.

The first reason for business failure is poor management and systems.

They are generally symptoms of poor leadership. Management systems, both financial, sales and operational that are robust, timely and accurate are essential to manage a business both on a day to day basis and for the long term. They enhance management’s capacity to understand what is occurring in the business.

The second reason why companies fail is related to the people in the business.

In particular those in leadership positions. For example, allowing egos to undermine the evidence by believing that everything positive is due to your talents and genius and anything negative is the result of another party or the government. This approach of internalising the positives of the business and externalising the negatives is not facing the brutal facts. Hubris and exaggerated outward confidence will mask the true situation of the business and hard decisions are not made.

In conclusion, while decreasing revenue, poor cash flow and opaque accounts may be a sign of a potential business collapse, these are often symptoms and warning signs of a potential business collapse.

The three questions you need to ask yourself are:

- Do you recognise the signs of a potential business collapse?

- Are your actions and attitudes part of the problem?

- What should I do now to prevent the risk of my business collapsing?